Podsumowanie

- What is Pillar 2 in Poland and which groups are within scope?

- Why does Pillar 2 in Poland require a separate analysis?

- Should a group bring FY2024 into scope for Pillar 2 in Poland?

- How can the FY2024 election be made in Poland?

- What reporting obligations does Pillar 2 create in Poland?

- What are the Pillar 2 reporting deadlines in Poland?

- Does the CbCR safe harbour solve the issue in Poland?

- What errors most commonly arise when implementing Pillar 2 in Poland?

- What should groups do now in relation to Poland?

What is Pillar 2 in Poland and which groups are within scope?

Pillar 2 in Poland is the domestic implementation of the EU and OECD global minimum tax framework designed to ensure that the effective tax rate of large multinational groups does not fall below 15% in any jurisdiction. In practice, the rules primarily apply to groups with consolidated revenue exceeding EUR 750 million and therefore also affect Polish entities that are part of foreign-headed groups. In Poland, the rules apply from 1 January 2025, although the legislature has also introduced an option to elect into the regime retrospectively for FY2024 through a specific formal process.

Why does Pillar 2 in Poland require a separate analysis?

Many groups initially assume that Poland is a high-tax jurisdiction and that exposure to top-up tax should therefore be limited. In practice, that assumption can be misleading. First, Poland applies a domestic minimum top-up tax, i.e. QDMTT, which means that any top-up tax may be collected locally in Poland before it is picked up at the parent level under the IIR. Second, the Polish tax environment is relatively incentive-heavy – R&D relief, the IP Box and exemptions available under PSI/SSE may reduce the effective tax rate under the GloBE rules. Third, even where the model, data and calculations are centralised at HQ level, local compliance obligations remain with the Polish constituent entities.

Ważny fragment

From a practical standpoint, the key point is that Pillar 2 in Poland is not limited to a central group-level calculation. Polish entities must manage the local notification, the QDMTT return, data readiness and the clear allocation of responsibility for dealing with the tax authorities in Poland. In first-year reporting, operational preparedness is often the decisive factor in managing risk.

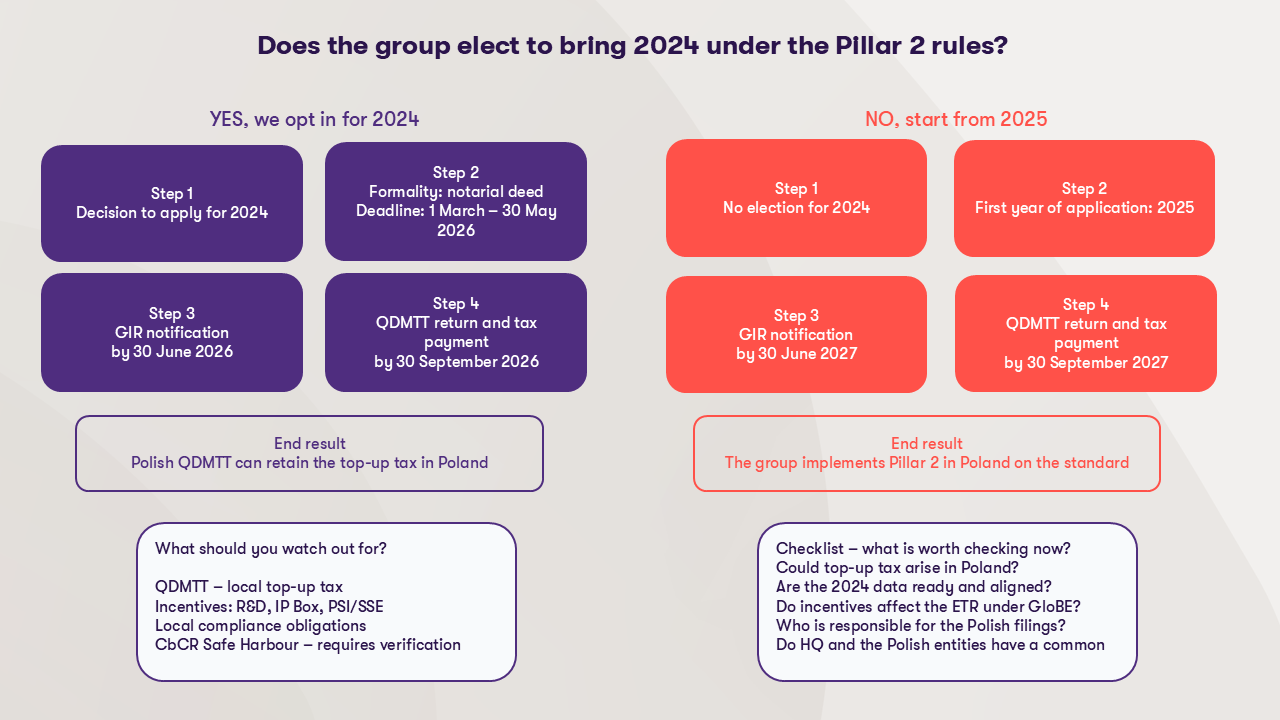

Should a group bring FY2024 into scope for Pillar 2 in Poland?

This is one of the most important decisions for groups with operations in Poland. FY2024 is not automatically covered – an active group decision is required in order to apply the rules retrospectively in Poland. Such an election may be justified where the group wishes to preserve consistency across jurisdictions, streamline the allocation of top-up tax or reduce the risk of losing reliefs such as the Transitional CbCR Safe Harbour. In practice, the decision is not only a compliance matter; it also has financial, governance and operational implications.

One of the principal benefits is that any top-up tax exposure may remain in Poland through the application of Polish QDMTT rather than being collected abroad at the level of the Ultimate Parent Entity. For some groups, the election also offers greater reporting consistency and a clearer local ownership model for Pillar 2 exposure in Poland. On the other hand, the election requires robust FY2024 data, formal alignment within the group and a clear assessment of whether Poland is in fact generating any top-up tax exposure.

How can the FY2024 election be made in Poland?

Retrospective application in Poland requires a formal statement executed in the form of a notarial deed. The filing window runs from 1 March 2026 to 30 May 2026, and the election is irrevocable. Where the Ultimate Parent Entity is located in Poland, it makes the election. Where the UPE is outside Poland, the process generally requires cooperation among the Polish constituent entities and the consent of the parent entity. In practical terms, this means that the group must align early on governance, documentation and timing if it intends to opt into FY2024 in Poland.

What reporting obligations does Pillar 2 create in Poland?

From the perspective of Polish entities, there are two key local obligations. The first is the notification identifying which entity will file the Global Information Return and in which jurisdiction it will be filed. The second is the local QDMTT return, i.e. the reporting of the domestic minimum top-up tax in Poland and, where relevant, its payment. This distinction is important because one global calculation does not translate into a single compliance obligation. HQ may prepare the GIR, but the Polish entities must still ensure that local compliance formalities in Poland are met.

In practice, there is a real risk that HQ focuses on the global filing workstream, while the local team identifies the Polish compliance steps too late. A further challenge is that dealings with the tax authorities in Poland take place locally and in Polish, which reinforces the need for clear ownership on the side of the Polish entities.

What are the Pillar 2 reporting deadlines in Poland?

If a group elects to bring FY2024 into scope in Poland and its financial year ends on 31 December 2024, the deadline for the GIR notification falls on 30 June 2026, while the deadline for the QDMTT return and payment in Poland falls on 30 September 2026. If the group does not opt for early application, the first year will, as a rule, be FY2025, and the equivalent deadlines in Poland will move to 30 June 2027 and 30 September 2027 respectively.

It should also be borne in mind that statutory deadlines are not the true start of the project. Auditors, CFOs and finance teams often ask about the Pillar 2 impact in Poland well before the formal filing deadline. For that reason, data analysis, validation of tax incentives and the allocation of process ownership should begin materially in advance.

Does the CbCR safe harbour solve the issue in Poland

The Transitional CbCR Safe Harbour may simplify the detailed calculation work, but it does not eliminate the need to understand the group’s position in Poland. Broadly, the simplification is based on three tests: the de minimis test, the simplified ETR test and the routine profits test. In practice, the group should not only verify whether the substantive conditions are met, but also ensure that Poland is correctly reflected in the reporting and that the available data can be reconciled with local statutory accounts in Poland. In the first year, the incorrect assumption that the safe harbour fully resolves the Polish position may have significant consequences in later years.

What errors most commonly arise when implementing Pillar 2 in Poland?

The most common issues usually arise not from tax theory but from process execution. Groups often analyse the FY2024 election in Poland too late, fail to reconcile CbCR data with Polish statutory accounts, do not model the impact of local tax incentives correctly, or assume that local reporting in Poland is fully covered by HQ. In addition, questions concerning financial reporting in Poland frequently arise before tax calculations are ready to support them.

What should groups do now in relation to Poland?

Ahead of the first filing deadlines in Poland, groups should carry out a practical readiness review. First, they should assess whether any top-up tax may arise in Poland and whether bringing FY2024 into scope has economic relevance. Second, they should verify whether data from Polish statutory accounts can be reconciled to the GloBE approach and whether local incentives – such as R&D relief, the IP Box or PSI/SSE exemptions – have been appropriately reflected. Third, they should designate a clear process owner on the side of the Polish entities for the notification, the QDMTT return, dealings with the tax authorities in Poland and coordination with HQ. Finally, they should monitor guidance issued by the Ministry of Finance and administrative practice in Poland, as this is where many practical execution issues are likely to emerge.

Pillar 2 in Poland now requires not only a sound understanding of the rules, but above all operational readiness for local reporting and the defence of the positions adopted in Poland. From a practical perspective, the most important point is that the FY2024 election, the global minimum tax assessment and data preparation for Poland should not be left until the statutory deadline. In our experience, an early and disciplined process set-up is what most often determines whether implementation in Poland is robust and manageable.